The Great Canadian Squeeze

Sovereign Substitution, Globalist Arbitrage, and Emergent Operational Architecture

For decades, the standard playbook for Canadian

enterprises,

operators, and

institutional investors

relied on a predictable set of assumptions:

stable North American trade corridors,

a predictable demographic baseline, and

an implicit sovereign backstop

that insulated the domestic economy from acute structural shocks.

Today, that playbook is obsolete.

Canada is caught

in an unprecedented macroeconomic bottleneck—

a structural squeeze

exploding statutory costs,

capital starvation, and

a dangerous sovereign attempt

to artificially subsidize

an uncompetitive domestic ecosystem.

For those building at the coalface

of markets and moonshots,

navigating this environment

requires moving past legacy planning.

It requires understanding

the exact fiscal telemetry

of the sovereign trap,

recognizing how global capital escapes it, and

deploying an agile, operational architecture

to survive and thrive amidst chaos.

The Sovereign Trap

The Macroeconomic Bottleneck

To understand the squeeze,

one must look directly at the sobering demographics and

statutory commitments of the Canadian state.

The baseline of the economy

is fundamentally compromised:

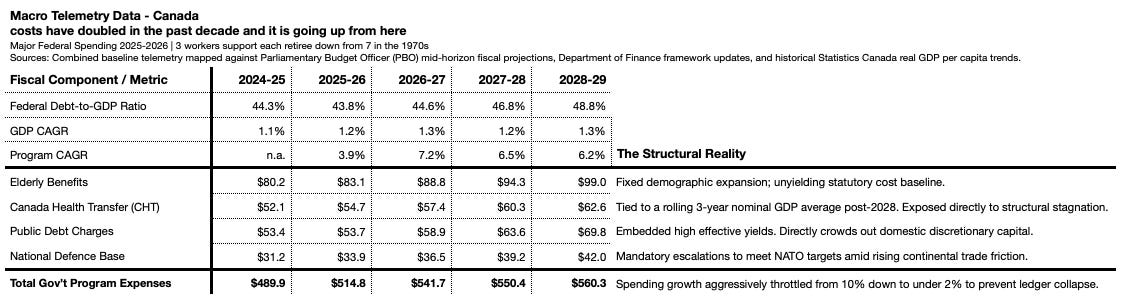

there are now only 3 workers

supporting each retiree,

a sharp drop from 7 in the 1970s.

This fixed demographic reality

enforces an unyielding statutory cost baseline

that no amount of short-term fiscal tinkering can bypass.

According to Parliamentary Budget Officer (PBO)

mid-horizon fiscal projections,

Elderly Benefits alone

are locked on a relentless upward trajectory,

expanding from $80.2 billion in 2024-25 to $99.0 billion by 2028-29.

Concurrently,

decades of accumulated debt

combined with higher structurally embedded interest rates

mean that Public Debt Charges

are surging from $53.4 billion to $69.8 billion

over the same horizon.

To prevent ledger collapse and

avoid a complete downgrade

of the sovereign debt rating,

the state is forced to aggressively throttle

total government program spending growth,

squeezing it down

to ensure statutory obligations

can be met.

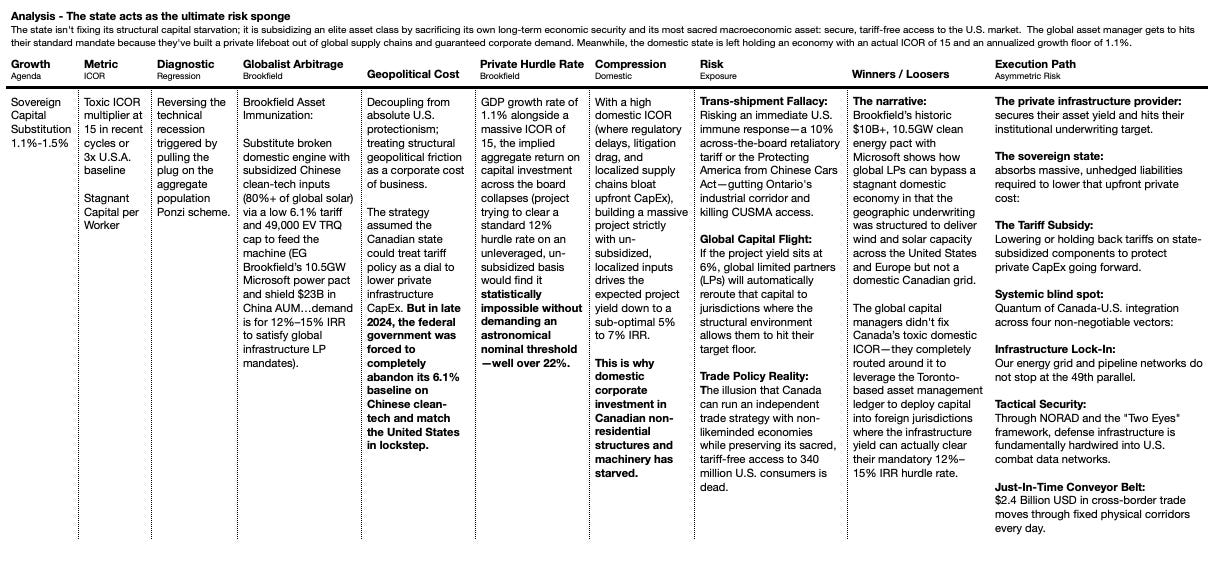

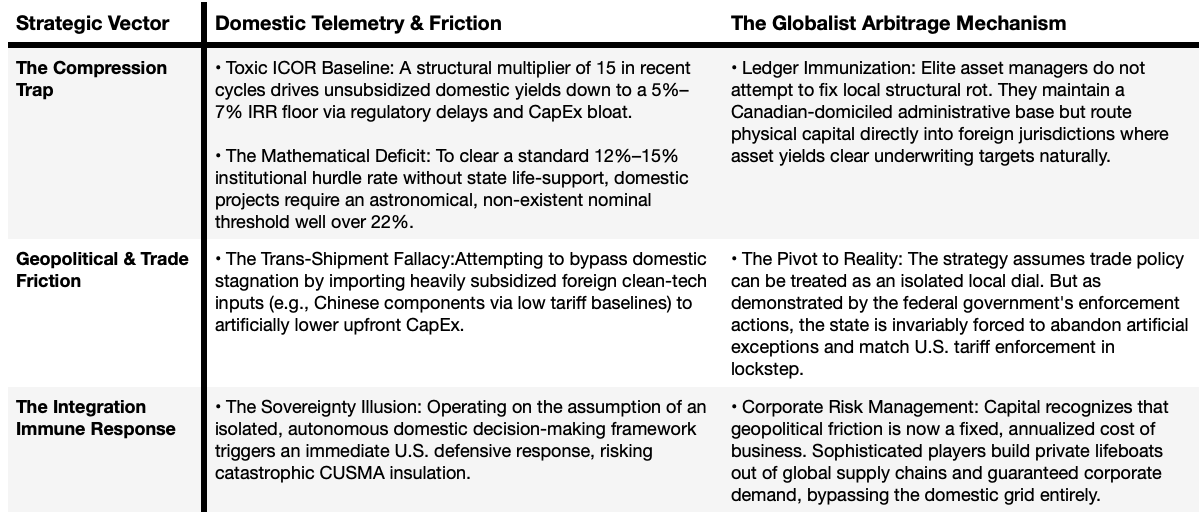

The Capital Trap and the ICOR Crisis

Compounding these demographic liabilities

is a catastrophic domestic capital investment crisis.

Canada suffers from a toxic

Incremental Capital-Output Ratio (ICOR)

of 15 in recent cycles—a measure of the capital required to generate a unit of output.

This ICOR is roughly

triple that of the United States,

meaning the Canadian economy

is incredibly inefficient

at turning capital investment

into tangible economic growth.

Regulatory drag,

litigation timelines, and

localized supply-chain friction

bloat upfront CapEx

to such a degree

that typical domestic projects

struggle to clear a meager 5% to 7% IRR.

Yet, to clear a standard institutional

unleveraged hurdle rate of 12% to 15%

in an environment with this level of friction,

projects would require nominal returns

that are practically non-existent in a

stagnant domestic market.

As a result, domestic corporate investment

in non-residential structures and machinery

is severely starved.

Globalist Arbitrage and the “Risk Sponge”

Faced with a toxic ICOR and sub-optimal domestic returns,

elite domestic and global capital managers

are executing a masterclass

in globalist arbitrage rather than attempting

to fix the domestic economy.

They use their Canadian-domiciled ledgers

as an administrative base,

but route their capital

directly into foreign jurisdictions

where infrastructure and energy yields

can actually clear their mandatory 12%–15% (UE / UK)

institutional underwriting hurdles.

A Story to Illustrate: The Ledger Stays. The Power Plant Doesn’t.

In mid 2024, Brookfield Asset Management —

headquartered in Toronto,

run substantially out of Canadian capital and

Canadian institutional relationships —

signed one of the largest clean energy agreements

in corporate history:

multi-billion-dollar,

10.5-gigawatt power deal

with Microsoft.

It’s the kind of announcement

that gets read as a Canadian win.

Canadian company,

historic deal,

clean energy,

AI infrastructure —

all the buzzwords line up.

The press release writes itself:

domestic champion,

global stage,

green transition,

the works.

Then you look at where the gigawatts are going.

The wind farms,

the solar arrays,

the grid interconnects —

all of it

is being built across the United States and Europe.

The asset manager is Canadian.

The capital pool drawing on Canadian pension and

institutional relationships is Canadian.

The 10.5 gigawatts of actual, physical,

steel-in-the-ground infrastructure is not.

Why the Power Plant Left and the Ledger Didn’t

Brookfield didn’t do anything wrong, and

didn’t do anything unusual.

It did exactly what a fiduciary

is supposed to do:

it found the jurisdictions

where the math works, and

it built there.

Understanding why requires walking through three layers —

the return gap, the routing logic, and

the state’s shrinking ability

to do anything about either one.

Layer One: Domestic Projects Don’t Clear the Bar

Large infrastructure investors —

pension funds,

sovereign-adjacent vehicles,

institutional limited partners,

operate under mandates that typically require

unleveraged returns

somewhere in the 12-15% range.

That’s not an aggressive target.

It’s closer to a floor:

the threshold below which a fund manager can’t honestly tell their own beneficiaries that the capital is working as hard as it should be.

A Canadian infrastructure project,

once you account for permitting timelines,

litigation exposure,

environmental review processes, and

the patchwork of provincial and federal approvals

layered on top of each other,

tends to land somewhere in the 5-7% range

on an unsubsidized basis.

That’s not a small gap.

It’s the difference between “fundable” and “not,” and

it’s a gap that exists before anyone has made a single bad decision

about the underlying project itself.

The wind is the same wind.

The sun is the same sun.

The difference is entirely in what it costs,

in time and dollars and legal exposure,

to get from “we’d like to build this” to

“this is generating revenue.”

Economists have a rough shorthand

for describing this kind of friction:

how much capital investment

a country needs

to produce one additional unit

of economic output.

By that measure, Canada currently needs

roughly three times what the US needs

to produce the same result.

Call it capital drag.

Call it regulatory friction.

Call it red tape

if you want the politically loaded version —

the practical effect is identical.

Every dollar of Canadian infrastructure capital

does less work here than the same dollar

would do somewhere else.

Not because the dollar is different.

Because the operating environment is.

Layer Two: When the Math Doesn’t Work, Capital Doesn’t Wait — It Routes

This is the part that’s easy to miss

if you’re reading the Brookfield deal

as a story about underinvestment.

It isn’t.

The natural assumption

is that Canadian infrastructure

is starved for capital —

that there’s a pool of money sitting on the sidelines,

waiting for permitting reform or political will or

some future government

to fix the friction described above,

at which point it will flow in.

That’s not what’s happening.

The capital isn’t waiting.

It’s already moved.

The Brookfield-Microsoft deal

isn’t capital failing to find a home in Canada.

It’s capital that found a home — just not here.

The ledger entry says Toronto.

The institutional relationships,

the reporting, the corporate registration,

all of it says Toronto.

The concrete says Texas, and Spain, and

wherever else the 10.5 gigawatts of wind and solar

are actually rising out of the ground.

This is worth sitting with,

because it inverts the usual framing.

The usual framing

treats Canadian capital flight

as a future risk —

something that might happen

if conditions don’t improve.

But the framing assumes

the capital is still here,

deciding.

It decided.

The decision already happened.

It happened at scale.

It happened through one of the most Canadian-identified

financial institutions in the country.

If the largest, most sophisticated,

most domestically-rooted pools of capital in Canada

have already concluded that the math doesn’t work here and

built somewhere else instead,

that’s not a warning sign about the future.

That’s a description of the present.

Layer Three: The State Tries to Close the Gap, and Runs Into Its Own Ceiling

Faced with projects

that can’t clear institutional hurdle rates

on their own,

the natural government response

is to subsidize the difference —

buy down the cost of inputs,

backstop construction risk,

narrow the spread between the 5-7%

a project can deliver unassisted and

the 12-15% an LP needs

to see before committing.

This isn’t a fringe idea or

a particular government’s pet project.

It’s the standard playbook,

used across political administrations,

because it’s the only lever available

that doesn’t require fixing

the underlying permitting and

litigation environment —

which is slow,

politically costly, and

involves dismantling things

that took decades to build up.

For a while, this works.

A subsidy here,

a loan guarantee there, and

a project that would have died at 6%

limps across the line at something closer to 12%.

The gap gets papered over, project by project.

But the room to keep doing that is shrinking, and

the reason is demographic,

not political —

which is precisely what makes it harder to argue with.

Canada has gone from roughly seven workers

supporting each retiree a couple of generations ago

to roughly three today.

That’s not a projection or a worst-case scenario.

It’s the current population,

doing what populations do,

arithmetically.

That shift shows up directly in the federal balance sheet,

in the most literal sense possible.

Statutory commitments like elderly benefits

are on a fixed upward trajectory that no government,

of any party,

of any ideological persuasion,

can simply choose not to pay.

These aren’t discretionary line items

that get debated in budget season.

They’re commitments made decades ago

to people who are retired now, and

the bill comes due regardless of what else

is competing for the same dollars.

At the same time, the cost

of servicing accumulated debt

is climbing as carrying costs

reset to higher rates than the debt

was originally issued at.

This, too,

isn’t a policy choice

in any meaningful sense —

it’s the mechanical consequence

of debt issued at one rate

needing to be refinanced

at whatever rate exists when it matures.

Put those two things together —

a statutory commitment

that’s legally locked in and growing, and

a debt-servicing cost

that’s mechanically resetting upward,

and you get a federal budget

where an increasing share

of every new dollar

is already spoken for

before anyone gets to decide

what to do with it.

Total federal program spending

is still going up in dollar terms;

that’s not in dispute.

But the growth rate of everything else —

the discretionary stuff,

the stuff that includes subsidies

for infrastructure projects

that can’t clear 12% on their own —

is being squeezed down hard,

because the non-negotiable stuff

is eating the increase before it arrives.

This is the ceiling.

Not a political ceiling

that a different government

could simply choose to remove, but

a structural one,

built out of demographic arithmetic and

interest rate resets,

that exists regardless

of who’s making the decisions.

Where That Leaves You

Domestic infrastructure projects

can’t clear institutional return thresholds on their own,

because of a return gap that’s structural rather than cyclical.

The state’s traditional tool

for closing that gap — subsidy — is drawing

from a pool of discretionary spending

that’s shrinking in relative terms every year,

for reasons that have nothing to do

with policy preference and

everything to do with demographics and

debt math that’s already locked in.

And the capital that the gap

was supposed to attract has already demonstrated,

at the scale of one of the largest energy deals

in corporate history,

that it doesn’t wait around for the gap to close.

It routes.

If you’re an operator, founder, or allocator

working on anything capital-intensive in Canada,

this isn’t background noise.

It’s the operating environment, and

it has three direct implications.

Don’t build a model that needs the gap closed by subsidy.

Government co-investment, grants,

and backstops are real, and

worth pursuing where available —

but they’re drawing from a pool

that’s contracting in relative terms every year,

regardless of which party is in office or

what they’ve promised.

A project that only works with the subsidy

is a project that stops working the moment

the fiscal envelope tightens further.

And the data says it’s going to tighten further,

on a timeline that’s largely already determined.

“Canadian-domiciled” is not the same as “Canadian-deployed.”

If part of your thesis involves attracting capital from

Canadian pension funds,

asset managers, or

institutional pools because they’re Canadian —

on the theory that domestic capital

has some kind of home-field loyalty —

Brookfield’s own deal is the counter-evidence.

The largest, most domestically-identified

Canadian capital pool in the relevant category

looked at a 10.5-gigawatt opportunity and

built it somewhere else.

The capital will show up

if your project clears 12-15%

on its own structural merits.

It won’t show up because

of where the head office is.

The gap itself is the opportunity.

Every one of these pressures exists

because something doesn’t currently exist:

a way to get a domestic project from 5-7% to 12-15% through structure, rather than through subsidy.

That’s not a reason

to write off Canadian infrastructure — it’s the actual brief.

The fiscal room to subsidize is shrinking

on a schedule that’s already written

into the demographic and debt data.

Whoever can close that gap

without leaning on a state that’s running out of room to help

isn’t fighting the trend the Brookfield deal represents.

They’re the answer to it.

The power plant left because the math told it to.

Nobody’s going to build the next one here by arguing with the math.

They’re going to build it by changing it.

This is part of the Good Turn Signal series —

distinguishing genuine signal

from performed noise

in governance, strategy, and public life.

The CUSMA Paradox and Sovereign Risk

This brings us to the ultimate strategic paradox and

the greatest threat to Canadian operators:

the trans-shipment fallacy.

Canada cannot run an independent,

opaque trade strategy with

non-likeminded economies

while simultaneously preserving

friction-free access

to the United States and its 340 million consumers.

The physical and digital integration

of the North American economy is absolute,

operating across three non-negotiable vectors:

Infrastructure Lock-In: Our energy grids, power pools, and pipeline networks are physically hardwired across the 49th parallel; they do not stop at national borders.

Tactical Security: Through NORAD and the “Five Eyes” intelligence-sharing framework, Canadian defense and communications infrastructure is deeply intertwined with U.S. combat data networks.

The Just-In-Time Conveyor Belt: $2.4 Billion USD in cross-border trade moves through fixed, highly optimized physical corridors every single day.

The Execution Path: Moving Past the Sovereign Trap

The structural reality of the Canadian macro-environment

is no longer a matter of forward-looking debate.

The data is in,

the decisions have been institutionalized, and

the telemetry is unyielding.

As mapped out

in the Sovereign Capital Substitution Matrix below,

the domestic state has increasingly defaulted

to acting as the ultimate,

unhedged risk sponge.

Faced with an annualized GDP growth floor

locked between a meager 1.1% and 1.3% and

a stagnant pool of capital per worker,

the sovereign is attempting to artificially

buy down structural liabilities

by sacrificing long-term economic security and

its most sacred macroeconomic asset:

secure,

friction-free access

to the U.S. market.

The Capital Substitution Matrix

The Three Non-Negotiable Vectors

For

operators,

founders, and

allocators

building at the coalface

of capital-intensive industries,

navigating this environment

requires an absolute rejection

of performed governance.

Any model built

on the assumption

of a fully isolated,

sovereign Canadian

decision-making sandbox

is fundamentally flawed.

Your operational architecture

must align directly with the three physical and

digital vectors

that hardwire the Canadian economy

to the U.S. demand sink—

corridors where trade moves

past national borders

at a rate of $2.4 Billion USD

every single day:

Infrastructure Lock-In: Energy grids, power pools, and pipeline networks physically integrated across the 49th parallel.

Tactical Security: Critical communications and defense frameworks fundamentally hardwired into U.S. combat data networks via NORAD and the Five Eyes intelligence alliance.

The Just-In-Time Conveyor Belt: Highly optimized, highly physical industrial corridors engineered for velocity, not administrative friction.

Changing the Math

The Brookfield-Microsoft pact

wasn’t a warning sign of future capital flight;

it was a execution diagnostic

of the present.

The largest, most domestically rooted pools

of capital have already concluded

that trying to paper over

an uncompetitive ecosystem

with shifting sovereign subsidies

is a terminal strategy.

When the underlying math

doesn’t work,

capital doesn’t wait around

for policy to catch up.

It routes.

The brief

for the next generation

of builders is not to build models

that rely on the state’s shrinking fiscal capacity

to absorb risk.

The brief

is to design structural mechanisms

that can drag a domestic project

from a 5% baseline to a 15% institutional yield

through sheer operational velocity,

regulatory immunization, and

hardwired integration

into global supply chains.

The power plant

left because

the math told it to.

Nobody is going

to build the next one here

by arguing with the telemetry.

We build it

by changing the architecture

of execution.